A Comprehensive Analysis of Emerging Risks, Market Dynamics, and Strategic Solutions for High-Net-Worth Individuals

The private client insurance landscape is experiencing unprecedented transformation driven by converging forces: escalating climate-related catastrophes, explosive cyber threats, nuclear verdict litigation trends, and the largest intergenerational wealth transfer in history. As we enter 2026, high-net-worth (HNW) individuals and families face a fundamentally different risk environment than existed even five years ago.

Key findings include:

- Climate-driven property insurance costs rose 10.4% nationally in 2024, with catastrophe losses reaching $176 billion

- Personal cyber risk exposure exploded 3,000% for deepfake fraud, with average U.S. breach costs exceeding $10.22 million

- Nuclear verdicts ($10M+) median awards reached $23.8M in 2023, creating liability insurance crises

- Baby boomers control $19.7 trillion in real estate (41% of U.S. total), creating complex transfer challenges

- Protection gaps widened significantly, with only 47% of catastrophe losses insured in 2024

For private clients, their advisors, and family offices, 2026 demands proactive risk management strategies addressing these interconnected exposures while navigating an increasingly complex insurance marketplace.

The Evolving High-Net-Worth Risk Landscape

Baby boomers control $19.7 trillion in U.S. real estate—41% of total value despite representing only 20% of the population[1]. This concentration, combined with aging properties and intensifying climate risks, creates unprecedented insurance challenges.

High-net-worth individuals face converging exposures: multiple properties across catastrophe-prone regions, valuable collections requiring specialized coverage, elevated liability risks from social inflation, complex estate structures demanding policy coordination, and growing cyber vulnerability as digital wealth management expands.

The insurance protection gap has widened dramatically. In 2024, U.S. catastrophe economic losses reached $176 billion while insured losses totaled only $99 billion—a $77 billion protection gap[2]. For private clients, this reflects underinsurance from rapid property appreciation, coverage exclusions for flood and earth movement, policy sub-limits, increasing carrier restrictions in high-risk areas, and, in some cases, the choice to self-insure.

1. Climate Change and Property Insurance Crisis

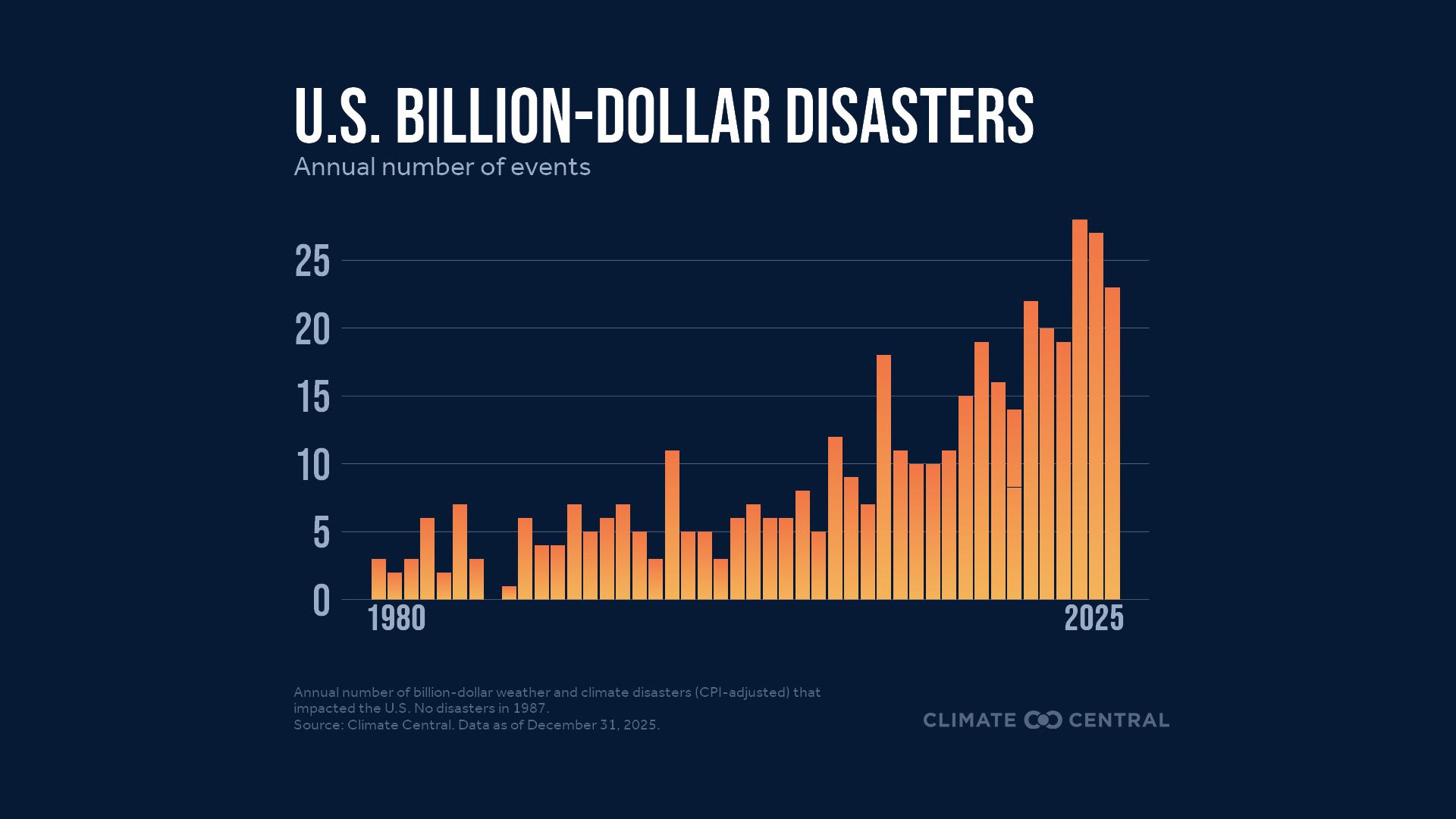

The year 2025 marked the fourth-warmest on record for the United States, with 27 weather disasters exceeding $1 billion in losses each[3]. Notable events included the Eaton and Palisades Fires destroying 18,000+ structures in Southern California, Texas Hill Country’s 1-in-1,000 year flood killing 135 people, and 1,559 tornado reports—fifth-highest on record[3].

Sea level rise has doubled from .06 inches to .14 inches annually, creating 3-9 times more frequent coastal flooding than 50 years ago[4]. Combined with accelerating drought (42.8% of U.S. affected per US Drought Monitor), these trends fundamentally reshape property insurability.[4]

Insurance Market Response:

Homeowners insurance rates increased 10.4% nationally in 2024, with six states exceeding 20%[5]. Major carriers withdrew from California, Florida, and Louisiana, forcing reliance on surplus lines (up 31.2% to $5 billion) and residual markets (up 6% to $10 billion)[5]. Carriers implemented percentage-based wind/hail deductibles, roof age restrictions, and tightened underwriting standards.

For HNW clients with multiple high-value properties, this creates acute challenges: limited carrier options, higher premiums, broader exclusions, and potential uninsurability in catastrophe-prone coastal and wildfire zones where many retirement properties are concentrated.

How to address:

Home Resiliency

- Prioritize loss‑prevention tools as these steps can improve insurance options and potentially reduce premiums:

- Water leak detection and automatic shutoff systems

Whole home backup generators

Annual or seasonal maintenance checklists to address minor issues before they become major

Coverage Options

Review your policy for exposures such as flood, earthquake, and sinkhole to determine whether adding these coverages makes sense based on where your home is located.

Acquisitions

- Consult your advisor before making an offer—especially for out of town or out of state home purchases. This helps you ask your realtor the right questions, improve insurability, manage long term costs and make educated buying decisions.

- Consolidating coverage with one carrier can enhance program efficiency, improve eligibility for better coverage, and ensure consistency across policies to prevent gaps or overlaps in coverage.

2. The Cyber Threat to Personal Wealth

Escalating Personal Cyber Threats

Ransomware Evolution

Ransomware was involved in 44% of all data breaches in 2024, with attacks shifting to “double extortion”—stealing personal financial records, tax returns, estate documents, and smart home data before encrypting systems and threatening public release[7].

The Deepfake Epidemic

AI-generated deepfakes exploded 3,000% in 2025, enabling unprecedented fraud targeting wealthy individuals[9]:

- Voice cloning of family members requesting urgent wire transfers

- Video impersonations of financial advisors authorizing transactions

- Synthetic identity creation for account takeovers

- AI-enhanced phishing with 54% success rates—quadruple traditional methods[10]

Shadow AI Risks

Household staff and family members using unauthorized AI tools (ChatGPT, Claude) for convenience create data leakage risks as personal information may be retained and exposed.

Cyber Risk Management Best Practices

Private clients should implement layered cyber defenses:

Technical Controls

- Multi-Factor Authentication (MFA): Strongly recommended for all financial accounts, email, cloud storage.

- Endpoint Detection & Response (EDR): Advanced antivirus/anti-malware on all devices

- Network Segmentation: Separate IoT/smart home devices from financial/personal computing

- VPN Usage: Virtual private networks for all remote/travel internet connections

Interactive Best Practices

- Wire Transfer Protocols: Verbal confirmation of all wire instructions via known phone numbers

- Email Authentication: Training to identify phishing, suspicious links, urgency-based manipulation

- Social Media Privacy: Limit disclosure of travel, property locations, purchases, family information

Coverage Coordination

- Review homeowners for any cyber coverage endorsements and what limits are available.

- Coordinate with any business cyber policies if working from home.

- Understand what is and isn’t covered.

3. Nuclear Verdicts and Liability Crisis

Nuclear verdicts—jury awards exceeding $10 million—have escalated dramatically. Analysis of 1,288 verdicts from 2013-2022 reveals median awards reaching $23.8 million in 2023 (up from $21.1 million), with mega verdicts ($100M+) increasing 400% since 2013[14].

Florida leads with 0.939 verdicts per 100,000 people—50% higher than New York. California, Florida, New York, and Texas produce half of all national nuclear verdicts[15]. State courts host 90% of verdicts versus only 10% in federal courts.

Critically, noneconomic damages (pain and suffering) drive verdict severity. In seven of ten years, noneconomic damages exceeded punitive damages, demonstrating susceptibility to psychological manipulation including “reptile theory” tactics, anchoring (suggesting arbitrary amounts that double to quadruple awards), and $1 billion in annual lawsuit advertising normalizing extreme awards[16][17][18].

Impacts on Private Clients

A 2025 Georgia jury awarded $4.2 million for a dog attack—far exceeding typical homeowners policy sub-limits of $100,000-500,000[19].

Making sure you have an appropriate umbrella limit is paramount. This limit of coverage is meant to be a moving target that is adjusted as your lifestyle evolves. Have a conversation with your advisor to discuss any significant changes in your net worth and/or public profile. Higher limits are available and we’re here to help.

4. Intergenerational Wealth Transfer Challenges

Baby boomers control $19.7 trillion in real estate, with the boomer population projected to decline 23% by 2035 and another 47% by 2045—transferring enormous holdings to millennial and Gen X heirs[21][22]. However, nearly 40% have lived in current homes 20+ years, with 68% in homes at least 30 years old[23]. Deferred maintenance—aging roofs, HVAC systems, electrical, and plumbing—often requires $50,000-$200,000+ in immediate upgrades inheritors lack funds to complete.

Insurance Complications

When aging parents move to assisted living, standard homeowners policies limit vacant property coverage to 30-60 days, requiring vacant home endorsements (30-50% higher premiums), regular inspections, winterization, and security monitoring. Failure to maintain proper coverage results in claim denials for theft, vandalism, or weather damage.

Post-inheritance, carriers increasingly restrict coverage on older homes through roof age limitations (declining roofs over 15-20 years), four-point inspections, wind mitigation requirements, and wiring restrictions. Inheritors may discover properties uninsurable without significant investment.

Multiple heirs create additional complications: disagreement on disposition, unequal contribution ability, mortgage difficulties, and liability exposure when one heir is judgment-proof while another has assets.

Many boomers retired to Sunbelt locations—Florida, California, Texas, Louisiana, Arizona—now facing acute climate risks. Millennial inheritors discover properties in locations they don’t want with deteriorating insurance availability. [26].

Avoiding Underinsurance (and Overinsurance)

- Choose carriers that use in home appraisals, apply annual inflation guards, and offer guaranteed or extended replacement cost. These protections help maintain proper insurance to value.

- If you haven’t appraised your fine art, jewelry, or collectibles in 3–5 years, schedule an updated review. Rising precious metal values mean some items may now be underinsured, while others may not require as much coverage and should be reduced which would provide a premium savings.

Asset Transfer Guidance

- Speak with your advisor before transferring assets to ensure proper risk management and insurance planning.

- Advisors can help prepare the next generation with education, loss prevention strategies, and insurance guidance.

- Homes: Discuss improvements that enhance home resiliency and insurability.

- Jewelry, fine art, wine/spirits: Review loss likelihood and proper insurance and risk management approaches.

- Middle market carriers often won’t insure high value items, or, in some cases, charge more for inadequate coverage.

- Asset transfers often indicate that the next generation needs a more sophisticated, high net worth insurance program.

- Working with a private client insurance advisor ensures proper coverage, carrier selection, and expert guidance.

2026 Market Outlook

The private client insurance landscape of 2026 is characterized by converging mega-trends which interact and compound and the need to adjust accordingly is evident.

Property insurance faces continued volatility with national average increases projected 8-12% for homeowners, and 15-25% on average in catastrophe-prone states (FL, CA, TX, LA).

Percentage-based wind/hail deductibles expand beyond coastal zones, roof age limitations tighten to 15-year maximums, and carriers reduce willingness to write vacant or secondary homes. However, reinsurance rates declined 6.6% at January 2025 renewals, bringing modest relief.

Personal cyber policies are becoming a standard need for all clients, with limits increasing in response to the increasing risk.

Umbrella/excess liability premium increases moderate to 5-10% in 2026 after prior 15-30% spikes. There is additional underwriting scrutiny on driver records, property maintenance, dog breeds, and water features.

Conclusion

As the private client insurance environment undergoes rapid and profound change, high net worth individuals face a level of complexity and exposure unlike any previous era.

Climate driven property volatility, surging cyber threats, escalating liability awards, and the massive transfer of aging assets across generations are reshaping both risk and insurability.

In this landscape, protection gaps widen quickly, traditional carriers offer fewer solutions, and the costs of inaction grow exponentially. The path forward requires proactive planning—strengthening property resiliency, modernizing cyber defenses, securing adequate liability protection, and preparing heirs with the right education and insurance structures.

By partnering with skilled private client advisors and adopting a coordinated risk management strategy, families can safeguard wealth, maintain insurability, and navigate the evolving challenges of 2026 and beyond with confidence.

We invite you to reach out with any questions as we’re here to provide recommendations, information and guidance.

Interested in learning more? Check out our Insights page for other relevant education topics.

References

[1] Redfin analysis (2025). Baby boomer real estate holdings. Business Insider.

[2] National Association of Insurance Commissioners. (2025). Natural Catastrophe Risk Dashboard Report, December 31, 2024.

[3] National Centers for Environmental Information (NCEI). (2025). Assessing the U.S. Temperature and Precipitation Analysis in 2025. NOAA.

[4] NOAA Climate.gov. (2025). Sea level change data. National Oceanic and Atmospheric Administration.

Climate Change: Global Sea Level | NOAA Climate.gov

Monthly Climate Reports | Drought Report | December 2025 | National Centers for Environmental Information (NCEI)

[5] National Association of Insurance Commissioners. (2025). Homeowners loss ratio and P&C combined ratio data. Natural Catastrophe Risk Dashboard Report. Natural Catastrophe Risk Dashboard Report.pdf

[6] Khalil, M. (2025, December 3). Cyber Insurance Statistics 2025: Key Trends & Data. DeepStrike. https://deepstrike.io/blog/cyber-insurance-statistics-2025

[7] Khalil, M. (2025). Ransomware involvement in data breaches. Cyber Insurance Statistics 2025. DeepStrike.

[8] Khalil, M. (2025). Ransom demand and payment dynamics. Cyber Insurance Statistics 2025. DeepStrike.

[9] Khalil, M. (2025). Deepfake fraud statistics. Cyber Insurance Statistics 2025. DeepStrike.

[10] Khalil, M. (2025). AI-enhanced phishing success rates. Cyber Insurance Statistics 2025. DeepStrike.

[11] Khalil, M. (2025). Business email compromise claim statistics. Cyber Insurance Statistics 2025. DeepStrike.

[12] IBM Security. (2025). Cost of a Data Breach Report 2025. Cited in DeepStrike Cyber Insurance Statistics 2025.

[13] IBM Security. (2025). AI and automation impact on breach costs. Cost of a Data Breach Report 2025.

[14] Silverman, C., & Appel, C. E. (2024, May). Nuclear Verdicts: An Update on Trends, Causes, and Solutions. U.S. Chamber of Commerce Institute for Legal Reform.

[15] Silverman, C., & Appel, C. E. (2024). Top states for nuclear verdicts analysis. Nuclear Verdicts Report. Institute for Legal Reform.

[16] Silverman, C., & Appel, C. E. (2024). Economic vs. noneconomic damage composition. Nuclear Verdicts Report. Institute for Legal Reform.

[17] Silverman, C., & Appel, C. E. (2024). Anchoring tactics driving nuclear verdicts. Nuclear Verdicts Report. Institute for Legal Reform.

[18] Silverman, C., & Appel, C. E. (2024). Lawsuit advertising impact on verdicts. Nuclear Verdicts Report. Institute for Legal Reform.

[19] PropertyCasualty360. (2025, April 16). Georgia jury awards elderly woman $4.2M for dog attack. https://www.propertycasualty360.com/2025/04/16/georgia-jury-awards-elderly-woman-42m-for-dog-attack/

[20] TransRe. (2024). Medical malpractice verdict analysis. Cited in Institute for Legal Reform Nuclear Verdicts Report.

[21] National Association of Realtors. (2024). Baby boomer real estate ownership analysis. Business Insider.

[22] Harvard Joint Center for Housing Studies. (2024). Baby boomer population decline projections 2025-2045. Business Insider.

[23] Leaf Home & Morning Consult. (2024). Survey of 1,000 baby boomers on home age and maintenance. Business Insider.

[24] Metz, J. (2025). California property tax implications of inheritance. Senior Homeowner Solutions. Business Insider.

[25] Yahoo Finance. (2025). State Farm refused to cover Florida man’s repairs on his Porsche—why the courts are now involved. https://finance.yahoo.com/news/state-farm-refused-cover-florida-095800478.html

[26] Fairweather, D. (2025). Chief Economist commentary on inherited property challenges. Redfin. Business Insider. Boomers are leaving their millennial Children with a huge headache — James Morris Homes

[27] S&P Global Ratings. (2024). Cyber insurance market outlook: Premiums projected to reach US$23 billion by 2026 amid stable industry conditions. Industrial Cyber.